The 2022 Recession Explained

The Coming Recession

Recession talks are hot. If you take a look at google trends, you’ll find the word “recession” has become quite popular over the last couple of months. So what does that mean for real estate? What does it mean for you?

What is a Recession?

Think of Gross Domestic Product as an economic snapshot that’s used to measure the size and growth of an economy. GDP refers to the total market value of goods and services produced in the United States. The unofficial definition of a recession is two consecutive quarters of negative GDP, meaning the economy is shrinking not growing.

Our government doesn’t subscribe to the unofficial definition of two negative quarters of GDP—That would be too simple, right?

The National Bureau of Economic Activity (NBER) considers multiple economic factors such as unemployment, personal income, GDP, and retail sales. Officially declaring a recession takes time. That’s because Federal reporting data always lags behind and NBER knows how to drag its feet. In the Great Recession of 2008, the committee took almost a year to declare the start of the recession.

What Happens to Rates and Home Prices During Recessions?

A recession is a decline in economic activity—it means businesses suffer, production declines, and folks lose their jobs. But how does that affect home prices? Home prices across the board are coming down, right?

Take a look at the chart above. The vertical gray lines represent recessions and the blue line represents the Federal Funds Rate (interest rates). Historically interest rates fall during recessions. That increases demand!

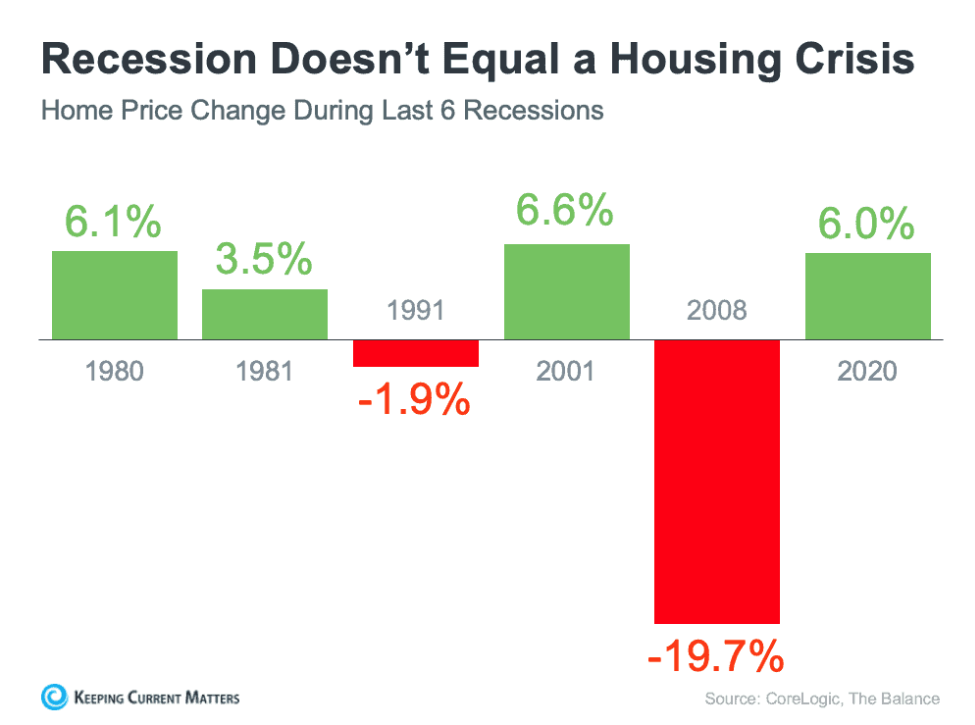

And if we look at the infographic below, we can see there’ve been six recessions in the United States in the last four decades. In four of those recessions, home prices actually appreciated.

What About 2008?

2008 is the giant elephant in the room. So let’s talk about it.

15 years ago, banks lowered lending standards and made it possible for virtually anyone to qualify for a home loan or refinance. Many purchasers weren’t truly qualified for the mortgages they obtained. The banks created artificial demand!

In today’s market, the demand is real. The worldwide pandemic generated a re-evaluation of the importance of home, and Millennials, the largest living generation, are quickly entering peak homebuying age and wanting to buy.

In 2008, homeowners turned their home equity into cash. It was normal for people to borrow against their homes to finance fancy vacations and new cars. When the prices dropped, those homeowners found themselves underwater and thought it was best to walk away. The Recession didn’t cause the mortgage crisis and housing crash. It’s the other way around.

In today’s market, folks are much more cautious. The amount of equity available for homeowners to access has more than doubled compared to 2006. People aren’t using their homes as piggy banks as they did leading up to the crash in 2008.

What Does This Mean for You?

If you’re a homeowner, you don’t need to worry about a real estate bubble popping. History tells us home prices appreciate during a recession. Although some areas might correct more than others. Perhaps areas that saw a temporary pump from the California migration, such as Arizona. But I’ll humor you, let’s say home prices do come down. Why do you care? It means the house you wanted to buy came down too, and you get a lower tax base.

If you’re a buyer, a recession means we can expect rates to come down. So you need to ask yourself. Would you rather wait for rates to come down and compete against other buyers? Or enter the market now, start building equity, and refinance when rates come back down? There’s no wrong answer.

The real question I want to know is: why are you interested in buying or selling? Real estate is inherently a great return on your investment. It’s also a reliable hedge against inflation and provides a variety of tax benefits. But let’s be honest, it was never to make money. It’s for freedom, confidence, security, and likely other values. Inflation, recession, interest rates—that’s all secondary.